Q3 2017 Highlights

01.

There continues to be strength and activity in the core market. The number of condo contracts signed with last asking prices between $1M - $3M and $3M - $5M increased by 11% and 7% year-over-year, respectively. This year-over-year increase in contract activity has been stimulated by a few macroeconomic factors: (1) equity markets, which are typically highly correlated with luxury residential sales in New York City, have continued to reach new highs (the S&P 500 increased by 17% year-over-year from September 2016 and recently crossed 2,500 for the first time), (2) financing remains readily available and inexpensive, and (3) purchasers now have the clarity needed to finalize buying decisions with confidence compared to a year ago when uncertainty regarding the U.S. Election, interest rate hikes, and Brexit was palpable.

02.

The ultra-luxury condominium market (+$10M) continues to face headwinds as a result of years of aspirational pricing. Although this quarter saw 31 contracts signed at a last asking price above $10M vs. 26 during 3Q16, it remains to be seen what the final taking price of these units will be, especially when considering that during 3Q17 $10M+ units, on average, traded at a 9% discount to original asking prices. Furthermore, 46% of all $10M+ units that sold this quarter required more than 180 days to find a buyer. Buyers at these price-points are aware of potential market softness and are exhibiting patience when trying to find an appropriately priced unit.

03.

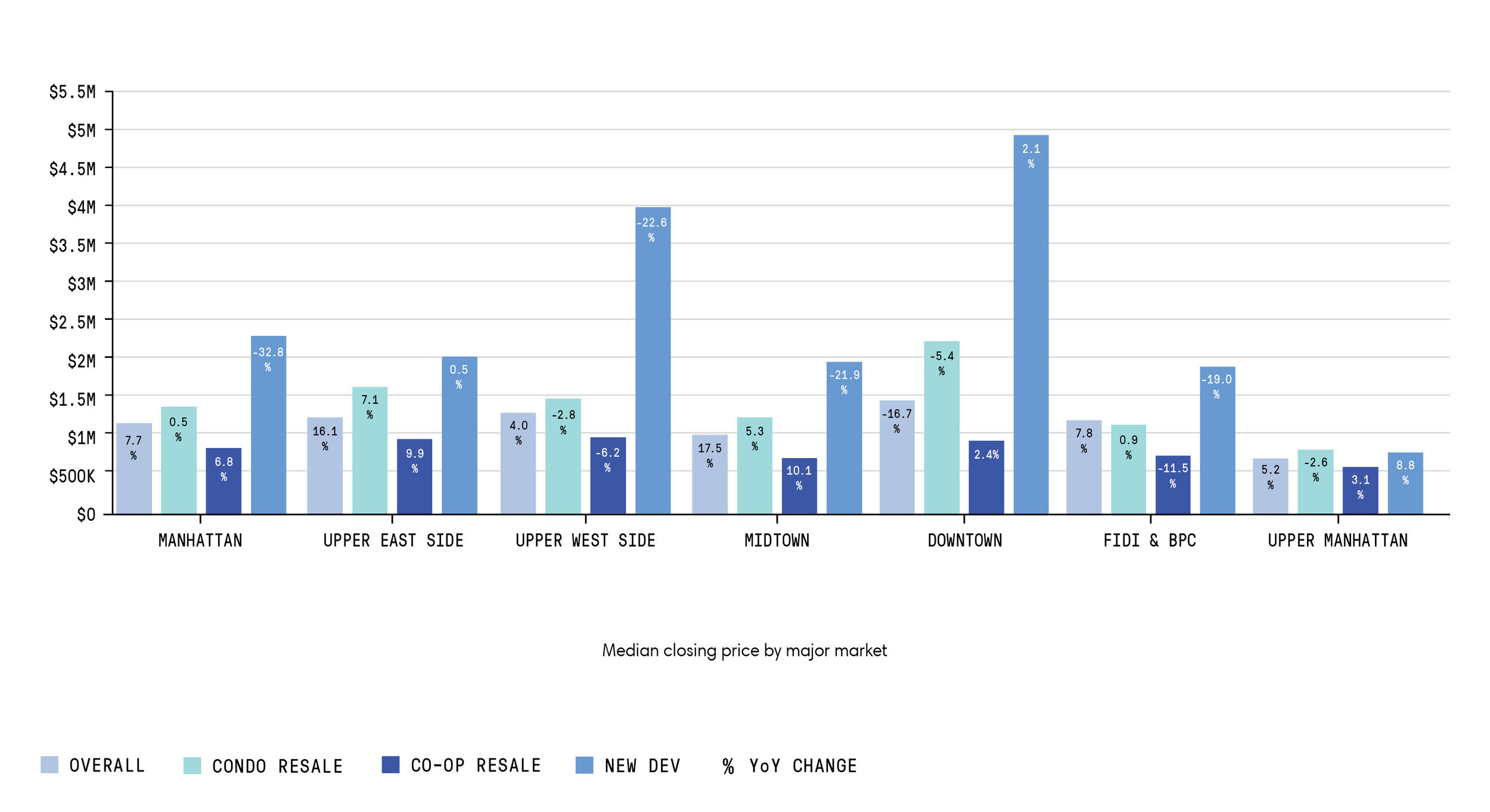

Although the median closing price for a new development condo in Manhattan declined by 33% year-over-year to $2.3M, we believe this market-wide metric is finally providing actionable and accurate price clarity into the new development market. In 2016 and early 2017, closings at long-awaited new development projects such as 432 Park Avenue, 56 Leonard, 30 Park Place, and The Greenwich Lane inflated the median new development price with transactions that had been signed in 2013 - 2014. Median closing prices are now less impacted by this ‘noise’ and are beginning to reflect a wave of newer developments with more attainable price points. Within the $1M - $3M price segment, there were 222 new development closings this quarter representing a 125% year-over-year increase.